Abstract

Despite the abundance of literature on agricultural price transmissions and unexpectedly disrupted value chains from infectious disease outbreaks such as bovine spongiform encephalopathy and COVID-19, the importance of research on price connectivity in the international beef markets has largely been ignored. To assess agricultural price transmission issues, error correction-type models (ECMs) have been predominantly employed. These models, however, suffer a deficiency in that the method is incapable of depicting time-variant linkages between prices. This article examines the connections between global and local prices, as well as price volatility in the beef sector. Our analysis uses a generalised autoregressive conditional heteroscedasticity (GARCH) model with the dynamic conditional correlation (DCC) specification that enables us to identify market connection intensity dynamics. We pay assiduous attention to structural changes in the overall research processes to enhance the reliability of estimation. For the first time in meat or grain price transmission research, our autoregressive models have been developed with structural break dummy variables for DCC. The principal findings are that (1) local retail prices for Azerbaijan, Georgia, Japan, Kazakhstan, Kyrgyzstan, Tajikistan and the UK showed a structural change in mean or variance, all of which were identified after the global food crisis from 2007–2009, (2) international prices unidirectionally Granger-cause regional prices in Georgia, Tajikistan and the United States in both mean and volatility (accordingly, no country exhibited price or price-volatility transmission from regional to international markets), and (3) volatility liaisons between global and local beef markets are generally weak, but price volatility exhibited closer synchronisation around the 2008 global food crisis, which created structural changes during the period. This finding implies that national governments should shield domestic from global markets by implementing trade restrictions such as quotas or taxes in a global emergency.

Similar content being viewed by others

Introduction

Price plays an important role in actualising efficient resource allocation in an economy. If high market efficiency is achieved, price oscillations are sensitively conveyed across markets. Price transmission research has long attracted economists seeking to elucidate market mechanisms to improve market efficiency. Consequently, a considerable number of articles on agricultural price transmission have been published, with approximately 500 articles resulting from an AgEcon database search with the keywords ‘price transmission’ (Kouyaté and vonCramon-Taubadel, 2016). However, relatively fewer publications centre on cross-border linkages (i.e., between global and domestic markets or between local markets in different countries), while the majority analyse price correlations within domestic markets (Ceballos et al., 2017). In particular, almost nothing is understood about the liaisons between international and regional meat markets even though meat value chains have been disrupted by infectious disease outbreaks such as bovine spongiform encephalopathy (BSE) and COVID-19. It is essential to elucidate market linkage mechanisms to mitigate such unexpected shocks to food security.

In past studies, analysis of agricultural price propagation issues predominantly employed error correction-type models (ECMs). These models, however, suffer from a deficiency in that the method is incapable of depicting time-variant links between prices. The dynamic conditional correlation (DCC) that originated from Engle (2002) facilitates observation of the intensity of market connections over time. This methodological process is frequently applied to price and price-volatility spillovers for financial markets such as equities, exchange rates and bond markets (e.g., Basher and Sadorsky, 2016; Gjika and Horvath, 2013; Gomez-Gonzalez and Rojas-Espinosa, 2019; Guo, 2018; Hou et al., 2019; Hwang et al., 2013; Kenourgios et al., 2016; Rizvi and Arshad, 2014; Shahzad et al., 2017; Shahzad et al., 2020; Tamakoshi and Hamori, 2013; Tamakoshi and Hamori, 2014; Tissaoui and Azibi, 2019). Furthermore, the application of DCC to energy issues can be seen in recent studies (e.g., Abdelradi and Serra, 2015; Abdullah and Masih 2016; Kaushik, 2018; Mensi et al., 2013; Mollick and Assefa, 2013; Naeem et al., 2020; Okorie and Lin, 2020; Pan et al., 2016; Sadorsky, 2014; Shiferaw, 2019; Vacha and Barunik, 2012; Xu et al., 2019; Zhang et al., 2017). The dynamic correlation process has never gained popularity in the literature on agricultural price transmissions.

A few articles tackle cereal price co-movement investigations, applying a DCC approach. For instance, Guo and Tanaka (2019) are the first to employ DCC to examine the relationships between world and local agricultural markets. Tanaka and Guo (2020) also utilised DCC to gauge the efficacy of wheat self-sufficiency policy measures for exporting countries. In addition, to the best of our knowledge, Guo and Tanaka (2020) is the only work that applied a time-varying correlation approach to international beef price passthroughs.

The importance of cross-border price co-movement research for the beef industry has been largely ignored, even though value chains (e.g., transport and food processing) have been disrupted by unexpected events such as BSE and COVID-19. However, the literature on price synchronisation within indigenous beef markets (i.e., relationships across farm-gate, wholesale and retail) is copious (Bakucs and Fertö, 2009; Boetel and Liu, 2010; Chang and Griffith, 1998; Dong et al., 2018; Fousekis et al., 2016; Goodwin and Holt 1998; Griffith and Piggott, 1994; Lloyd et al., 2006; Pozo et al., 2013; Saghaian, 2007; Sanjuan and Dawson, 2003). Although Dong et al. (2018) analyse regional market associations among Australia, China, Indonesia and Vietnam, they do not inspect the links with the global market. Ghoshray (2011) is the only work that delves into international beef market liaisons, covering a wide range of commodities and countries. However, regarding the beef sector, Ghoshray only analyses the Thai domestic market. Therefore, Guo and Tanaka (2020) is currently the only comprehensive analysis focusing on international price or price-volatility transmission for the beef sector.

Managing structural breaks is vital to enhancing the accuracy of estimators in a time-series analysis. Several existing studies on beef price co-movement considered structural breaks in their model estimations (Bakucs and Fertö, 2009; Chang and Griffith, 1998; Fousekis et al., 2016; Hernandez-Villafuerte, 2008; Lloyd et al., 2006; Sanjuan and Dawson, 2003). Cappiello et al. (2006) demonstrated the first application of structural changes to the DCC and asymmetric DCC. However, none of the past price transmission analyses for cereal commodities using the DCC diagnose structural breaks in time-variant correlations (Ceballos et al., 2017; Guo and Tanaka, 2019; Tanaka and Guo, 2020).Footnote 1 The present article thoroughly scrutinises the price interconnectivity between world and local beef prices for nine net importing countries, using GARCH-type models with the DCC specification. Our sample period ranges from January 2006 to May 2020. Applying the cross-correlation function (CCF)Footnote 2, we detect Granger causal relationships between global and local prices in both the mean and variance. We pay assiduous attention to structural changes in every estimation process (i.e., the unit root test, the estimation of both GARCH and DCC models) to gain more precise results.

The current analysis contributes to the literature empirically and methodologically. First, we uncovered the directions of cross-border beef market linkage mechanisms, using the Granger causality technique with carefully selected models based on the Bayesian information criterion (BIC) and accounting for structural breaks. Second, to our knowledge, this paper is the first in meat or grain price transmission research to develop autoregressive (AR) models for DCCs with structural breaks. The existing meat price transmission literature has largely adopted conventional methods such as ECM for analysis, which does not allow for visualising the intensity of market liaison dynamics. To resolve this analytical deficiency, we apply the DCC technique to beef price associations.

The paper is organised as follows. The following section explains data used in the analysis. Section 3 describes the specifications of the models we employed. Empirical results obtained from the models are delineated in Section 4. Finally, the paper is summarised with a discussion of the results.

Data description and preliminary analysis

This research concentrates on nine net beef-importing countries (Azerbaijan, Georgia, Japan, Kazakhstan, Kyrgyzstan, Tajikistan, Tunisia, the UK and the United States of America). These nations were selected based on data availability and the criterion that self-sufficiency in beef does not exceed 100% according to data sourced from the Food and Agriculture Organization (FAO) corporate statistical database (FAOSTAT). We collected monthly international and local retail beef price series for each country over the period from January 2006 to May 2020 in US dollar terms. The regional price data series for Azerbaijan, Georgia, Kazakhstan, Kyrgyzstan, Tajikistan and Tunisia was retrieved from the FAO global information and early warning system (GIEWS).Footnote 3 Data for Japan, the UK and the United States were acquired from the Agriculture & Livestock Industries Corporation (Japan), the UK Office for National Statistics, and US Bureau of Labor Statistics, respectively. For Japan and the UK, price data for local currencies were converted into US dollar equivalents with exchange rates obtained from Federal Reserve economic data.Footnote 4

To eliminate the influence of seasonal fluctuations, all beef price series are adjusted using the X-13-ARIMAFootnote 5 method. The monthly returns are calculated as the first differences of monthly logarithmic prices Rt = ln(Pt)−ln(Pt−1), where Rt is the monthly beef price return at time t, and Pt is the beef price at time t. The summary statistics for all beef price returns under investigation are displayed in Table 1. According to Table 1, Tajikistan shows the highest returns in mean and median, while Japan displays minimal mean and median values. However, the table indicates that the returns of international beef prices are more volatile than all the domestic prices, evidenced by the largest standard deviation. Meanwhile, Japan’s price returns also show relatively higher standard deviation than other countries. Note that the skewness values are all negative except for Tunisia and the United States, indicating there is a longer tail on the left side of the probability density function and a higher probability of observing negative rather than positive returns in most of the price returns. Furthermore, the high values of kurtosis for all the price returns suggests the existence of fat tails in the return distributions. All returns (apart from Tunisia) are not normally distributed, as indicated by the Jarque–Bera statistic. Finally, low and positive unconditional correlations between international and domestic beef prices are revealed, except for Azerbaijan. Specifically, the price return of Tunisia has a relatively high positive correlation and Japan has low correlation with international prices.

The returns of each beef price are plotted in Fig. 1. International and local beef price show considerable variability in the sample period and exhibit different patterns across different countries. For instance, some price returns (e.g., International price (henceforth, IP), Georgia, Japan and Kazakhstan) changed dramatically during turbulent periods, such as the global food crisis and great recession of 2007–2009. Furthermore, significant fluctuations in the price returns of Azerbaijan, Kazakhstan, and Tajikistan have also occurred during other periods, such as 2014–2016. These facts are reflected in beef return figures in periods of high volatility. The insights deduced from beef price returns may be indicative of structural changes in the data series, which will be examined in the analysis below.

Time-series plots of monthly beef price returns.

Before constructing the econometric model, a stationary process of each price return is tested using the augmented Dickey–Fuller (ADF)Footnote 6 and Kwiatkowski–Phillips–Schmidt–Shin (KPSS)Footnote 7 unit root tests. Table 2 reports the results of the unit root tests, which indicate that all price returns are stationary in their first log-differenced forms.Footnote 8 In addition, the main weakness of traditional unit root tests is that they do not account for endogenous structural breaks. Biased results may be seen when structural breaks impact the data series, as documented above in Fig. 1. Considering this, we apply Zivot and Andrews (1992) and Perron (1997) tests, which have the advantage of allowing for one unknown structural break in the price returns.

Table 2 shows the results of unit root tests with a break and presents the break date endogenously determined by the tests. According to Table 2, results of unit root tests with a break can be detected, which are similar to the usual unit root tests, suggesting that all beef price returns can be deemed as a stationary process. Moreover, turning our attention to the structural break identified for each price return, some estimated break dates correspond to the period of the food crisis and great recession of 2007–2009 (e.g., Georgia, Japan and the UK). The other break dates detected in the test occurred during the period 2014–2016.

In brief, preliminary analysis indicates that these price returns are characterised by non-normal distributions, negative skewness, fat tails, stationarity and an endogenous structural break. Based on these results, it is important to further examine the existence of multiple structural changes in the conditional mean and variance for each price return. GARCH-type models with structural break, CCF and DCC methodology are used to investigate Granger causality and the dynamic interaction between international and domestic beef prices in beef-importing countries.

Methodology

Given two stationary series {Xi,t}, i = 1, 2 and t = 1, \(\ldots \,,\) T where T is the sample size. Let Ωi,t be two information sets defined as Ωi,t = (Xi,t=j, j ≥ 0), i = 1,2 and Ωt = Ω1,t∪Ω2,t. Following Hong’s (2001) null hypothesis, X2,t Granger-causes X1,t in the mean if:

Meanwhile, X2,t is considered to cause X1,t in variance if:

where μ1,t is the mean of X1,t conditioned on Ω1,t−1.

To assess Granger causality between international and local beef prices in beef-importing countries, Hong’s (2001) non-uniform weighting CCF was applied. One of the key advantages of this approach is that it can detect the leading and lagging structures of causality, as well as the duration over which causality is exerted.Footnote 9 Specifically, based on the estimated GARCH-type models, the standardised residuals and the standardised squared residuals for international and local beef prices will be estimated, respectively. Next, the sample cross-correlation coefficient \(\widehat o_{12}\left( j \right)\) between the standardised residualsFootnote 10\(\left\{ {\widehat \vartheta _{i,t},\,t = 1,\,...\,,\,T} \right\},\,i = 1,\,2\) with lag j (j = 0, ±1, ±2, \(\ldots \,,\) ±(T−1)) can be represented as follows:

where \(T^{ - 1}\mathop {\sum}\nolimits_{t = 1}^T {\widehat \vartheta _{1,t}^2}\) and \(T^{ - 1}\mathop {\sum}\nolimits_{t = 1}^T {\widehat \vartheta _{2,t}^2}\)are the sample variances of ϑ1,t and ϑ2,t, respectively. Following Hong (2001), the causality-in-variance test statistics can be defined as:Footnote 11

where

If the test statistic Φ in Eq. 5 is larger than the upper-tailed critical value of N (0, 1), we reject the null hypothesis of no causality-in-mean or causality-in-variance during the first S lags.

Since the results of the CCF approach rely on the correct selection and specifications of the GARCH model applied, in this article we estimate the squared standardised residuals of each variable using three different types of GARCH models. Specifically, besides the univariate GARCH model, our analysis employs both the exponential generalized autoregressive conditional heteroscedastic (EGARCH)Footnote 12 and the Glosten, Jagannathan and Runkle-GARCH (GJR-GARCH)Footnote 13 models to capture the presence of asymmetry in volatility. The empirical model for international and domestic beef price returns can be specified as follows:

Equation (8) specifies the conditional mean equation, where Rt is the beef price return and the error term υt is assumed to follow a conditionally normal distribution with its conditional variance ht. Equations (9–11) represent the variance equations specified by the GARCH, GJR-GARCH, and EGARCH models, respectively. The indicator function Π−t-i in Eq. (10) equals 1 if υt−i < 0, and 0 otherwise. q is the number of GARCH terms, and p is the number of ARCH terms that can capture asymmetric effects. We carry out the lag selections using the BIC and determine the optimal univariate model for each price return.

Lamoureux and Lastrapes (1990) suggest that structural breaks in conditional variance may confound the estimation of a GARCH model, and that structural breaks should be incorporated into a GARCH model to obtain certain estimators. Moreover, argue that pre-testing needs to be executed for structural breaks in volatility before examining the causality-in-variance. In this regard, we employ Bai and Perron’s (2003) testFootnote 14 to identify the structural breaks in mean and variance equations. First, we apply this approach to the AR model and identify the structural break points in the conditional mean equation. Then, the residuals can be obtained from this estimation process. Next, we identify the structural breaks in the variance through the following equation:

where the transformed residual on the left-hand side indicates the unbiased estimator of the standard deviation of υt from the conditional mean equation. Moreover, c and ut are the constant and error term, respectively.

Finally, we use a bivariate GARCH model with a conditional variance-covariance matrix to estimate the DCCs between international and domestic beef prices and examine the volatility transmissions for each price pair. Following Engle (2002), we construct an econometric framework for the GARCH-DCC model, which was formulated as follows:

where

where Rt is a 2 × 1 vector of returns including the international beef price R1,t and domestic beef price R2,t. Ξt−1 is an information set at time t−1. υt = (υ1,t,υ2,t)′ is the vector of innovations, Ht is a 2 × 2 conditional variance-covariance matrix, ϑt is a 2 × 1 independent and identically distributed (i.i.d.) vector of standardised residuals. Θt is the diagonal matrix containing the conditional standard deviations of each price return. Λt is the time-varying conditional correlation matrix and Qt is the conditional correlation matrix of the standardised residuals, which can be defined by

where parameters a and b are non-negative, with a restriction of a + b < 1 to ensure stationarity and a positive definiteness of Qt. \(\overline Q\) is the 2 × 2 unconditional correlation matrix of the standardised residuals ϑt. Cappiello et al. (2006)Footnote 15 modified the correlation evolution by introducing the presence of asymmetries into the DCC model. The authors constructed an asymmetric generalised DCC (AG-DCC) model, as in the following expression:

where A and B are 2 × 2 parameter matrices. \(\overline N\) represents the unconditional matrices of ξt = I[ϑt < 0]⊗ϑt (I[·] is an indicator function equal to 1 if ϑt < 0 and 0 otherwise, while ‘⊗’ indicates the Hadamard product) and \(\overline N = E\left[ {\xi \xi ^\prime } \right]\). The asymmetric DCC (A-DCC) is a special case of the AG-DCC if the matrices are replaced by scalars. Moreover, if matrix G in Eq. (18) equals zero, then the generalised DCC model (G-DCC) can be obtained. Thus, the DCC ρij,t can be defined as:

The parameters of the DCC, A-DCC, AG-DCC, and G-DCC model are estimated by the Gaussian quasi-maximum likelihood estimation (QMLE),Footnote 16 assuming conditional multivariate normality with the BFGSFootnote 17 optimisation algorithm. Following Engle (2002), the likelihood function can be expressed as:

The parameter in matrix Θt and matrix Λt are denoted as η and ς, respectively. Finally, to determine the best of the four DCC models considered above, we examined the appropriate ability of each model using the BIC.

Empirical results

Identification of structural breaks and estimation of GARCH-type models

As explained in the methodology section, before examining the Granger causality and the dynamic relationship between international and domestic beef prices, the existence of structural breaks in the mean and volatility for each price return needs to be explored. Table 3 reports Bai and Perron’s (2003) unknown structural break test for beef price returns. According to Table 3, the scaled F-statistic indicates that there is no structural change in either the mean or variance for IP, TUNFootnote 18 and USA. However, it can be verified that GEO or KYR has a single break in the mean, and the identified break dates are March 2012 and October 2011, respectively. Note that two breaks occur in the mean of KAZ (January 2014 and February 2016) and TJK (July 2012 and August 2014). Table 3 also reveals that only one break exists in the variance of JPN (January 2010) and the UK (September 2014). Moreover, for AZE, there is only one break in the mean (February 2016) and two breaks in variance (March 2015 and April 2017).

Interestingly, structural breaks were not detected during the global food crisis (2007–2009), but after the event (i.e., 2010–2017). This may represent that domestic beef markets are less sensitively influenced by external markets. That is, internal factors could have caused the structural changes—at least for the sample countries. As seen in the later experimental outcomes, we demonstrated that the interlinkage between global and local prices in the beef sector is relatively weak. Since the structural break dates are identified in the mean and volatility of several beef prices, it is reasonable to incorporate their corresponding dummy variables in the estimation of GARCH-type models. Based on the model selection criteria,Footnote 19 we choose the best-fitting model for each price return. Table 4 provides the details about the model selection. The specification of the original GARCH (1, 1) model is selected for IP, AZE, KYR, UK, and USA because it had the lowest BIC value and highest log-likelihood ratio. The EGARCH (1, 1) model is selected for GEO, JPN, KAZ, and TJK. The GJR-GARCH (1,1) model is found to be best-suited for TUN.

The parameter estimates for univariate GARCH specifications are summarised in Table 4. Results indicate most of the coefficients of the ARCH (α1) and GARCH (β1) are statistically significant, thereby providing evidence of volatility clustering. The results were also confirmed with the near-unity sum of the estimated GARCH and ARCH terms for each price. Moreover, we can see a large magnitude of ARCH terms for TJK and JPN, which indicates that past shocks significantly impact the current conditional volatility in these two countries. However, the GARCH term measures the impact of past volatility on current conditional volatility. A relatively larger magnitude of the GARCH terms can be identified for TUN, UK, GEO, and KYR, which implies the persistence of volatility in these countries. Furthermore, it is noticeable that the asymmetric (γ) terms are statistically significant in the price returns of JPN. This result suggests that the asymmetric effect or ‘leverage effect’Footnote 20 is exerted on Japan’s price returns. Furthermore, the dummy variables are statistically significant in mean and variance for AZE, GEO, JPN, KAZ, KYR, TJK, and UK. These findings suggest that the dummy variable accommodates the structural change in the mean and variance of beef prices in these countries. Table 4 also shows the diagnostics of the empirical results for each model. The Ljung–Box statistics and ARCH-LM (Lagrange multiplier) tests show the null hypothesis of no autocorrelation. ARCH effects cannot be rejected at the 1% significance level for all price returns. The well-fitted mean and variance equations described above led us to conclude that our selection of AR-GARCH-type models fit the data reasonably well.

Causality-in-mean and Causality-in-variance analysis

Next, we examine the causality-in-mean and variance and lead-lag relationship between international and domestic beef prices by using the standardised residuals obtained from each GARCH-type model. Since the CCF-based approach is typically applied to investigate the causal relationships in a bivariate framework, we present the empirical results for each pair of international and domestic prices. We use Hong’s (2001) statistics to test the null hypothesis of no causality from lag 1 to lag M (5, 10, 15) month. The results of causality-in-mean are reported in Table 5. Overall, it is somewhat interesting to ascertain that different causality exists across different countries. We can verify that a unidirectional causality-in-mean runs from IP to domestic prices for GEO, JPN, KAZ, TJK, and the USA. Specifically, IP Granger-causes these domestic prices with a one-month lag up to a 5-month lag, suggesting that the domestic beef market exhibits a speedy reaction to change in the global beef price. In contrast, the reverse causality is not significant, which implies a leading role of the international beef price regarding price transmission. That is, excessive volatility in international beef prices would increase the uncertainty of the domestic beef market in these five countries. However, it can be observed that there are no causality-in-mean effects between IP and domestic prices in AZE, KYR, TUN, and UK. Thus, there is no evidence of price information transmission and contagion between IP and local prices in these four countries

As for the causality-in-variance test, the results are reported in Table 6. Comparing the results with Table 5, we note several interesting findings. First, similar to causality-in-mean, there was no explicit causal relationship between IP and beef prices in AZE and TUN. Thus, information links between international and local prices in these two countries are weak and correlation between them is low. Second, different characteristics of spillover effects from volatility are found between international and domestic prices. Specifically, From Table 6, we can see that there is no statistically significant evidence of causality-in-variance effects between IP and domestic prices in JPN and KAZ, which is different from those in the results of causality-in-mean. Moreover, it is interesting to identify a unidirectional causality-in-variance from IP to domestic prices in KYR and the UK, which does not have causality-in-mean effects. These results provide evidence of one-way lead-lag volatility spillovers from international beef prices to these two countries’ local beef prices. Furthermore, IP Granger-causes UK and USA with ten-month and fifteen-month lags, indicating that a delayed reaction and longer time is needed for volatility transmission for these two countries. In sum, our findings confirm the existence of a causal linkage either in mean or in variance from international beef prices to local beef prices in GEO, TJK, and the USA.

Our Granger linkage outcomes indicate that any of the importing nations do not affect the international price of beef, whereas indigenous prices in Georgia, Tajikistan and the United States are influenced by global prices both in mean and variance, which implies closer interconnections with the international market. Note the mean of the beef self-sufficiency rate (SSR) of Georgia, Tajikistan, and the United States during the sample period was 74, 98, and 97%,Footnote 21 respectively, which is not necessarily lowFootnote 22 although it is widely recognised that the food autarky measure contributes to segregating domestic from foreign markets (Guo and Tanaka, 2019; Tanaka and Guo, 2019; Tanaka and Guo, 2020).Footnote 23

Time-varying conditional correlations

In the next step, we estimate the time-varying conditional correlations between international and local beef prices. First, we should select the most appropriate model of four DCC specificationsFootnote 24 for each price pair. The results of the model selection in Table 7 show that the standard DCC model is selected as the best fit for IP vs. AZE, IP vs. JPN, IP vs. KAZ, and IP vs. KYR and IP vs. TJK. The G-DCC model is selected for the pair of IP vs. GEO, IP vs. UK, and IP vs. USA. However, the A-DCC model is selected for IP vs. TUN, and AG-DCC is not suitable for any price pairs. The parameters for all the selected models are estimated by maximising the log-likelihood functions mentioned in the methodology section.Footnote 25

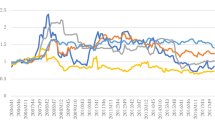

Finally, we address the issue of global-local market linkages based on the DCCs between international beef prices and those of nine beef-importing countries. The evolution of DCCs is plotted in Fig. 2 for all the pairs of prices. First, although DCCs exhibit some different patterns across different countries, several similar characteristics of the depicted pairwise correlations are that most of them change visibly over the sample period and show evidence of upward and downward peaks at some common times. Specifically, it can see that DCCs in some countries (e.g., AZE, GEO, JPN TJK, TUN, and the UK) fluctuated dramatically during 2007–2008, which may be explained by the turmoil characterising the global food and financial crisis over the period. For instance, we observe that DCCs of Japan record an increase almost until the end of 2007, then drop dramatically from early 2008, and return to their path from mid-2009. These features suggest the food crisis had significant impacts on the interrelationship between international beef prices and domestic prices in these countries. Moreover, similar trending patterns are observed in the period of 2014–2015 for AZE, GEO, JPN, and the UK. These countries tended to show sharp declines in the 2014.

Plots of time-varying conditional correlations.

Second, we focus on the sign of DCCs between international and domestic prices. Note that the DCCs of JPN, KAZ, and the UK show some negative values throughout the entire sample period and a relatively high level of magnitude. These results can be explained by a lead-lag information transmission across global and local beef markets. Our empirical results in the previous subsection detect a unidirectional causality between international and local prices in JPN, KAZ, and the UK. Therefore, it is reasonable to assume that increases or declines in international beef prices will bring about lagged increases or declines in domestic beef prices in these three beef-importing countries.

Third, as can be observed, the extent of the positive values in DCCs is relatively low in some countries (e.g., GEO, TJK, and the USA). These features indicate weak price transmission and volatility spillovers across the international and domestic beef markets in these countries.

In addition, we report descriptive statistics of DCCs for all countries in Table 8. We find that the magnitude of the mean of DCCs range from −0.099 (JPN) to 0.210 (KYR). Moreover, the median of DCCs range from −0.109 (JPN) to 0.213 (KYR). As can be seen, the maximum value of DCCs is 0.999 for the United States and the minimum value of DCCs is −0.755 for KAZ. These findings reveal different variations of DCCs across various countries. Moreover, DCCs of AZE exhibit larger fluctuations than the other countries, thus demonstrating the highest standard deviation (0.258). In contrast, GEO has the most stable DCCs, evidenced by the lowest standard deviation (0.062). Overall, the results suggest low global-local market linkages between international beef prices and domestic prices in beef-importing countries. These may be explained by the characteristics of SSR and food policy in each country.

Effects of structural breaks on correlations

As documented in Fig. 2, the DCCs seem to be characterised by structural shifts over time in some beef-importing countries. Such findings motivated us to conduct a detailed investigation on whether there are structural changes in estimated dynamic correlations and its effects. First, we use Bai and Perron’s (2003) structural breaks test to identify the number of break points and their locations in each DCC. Table 9 provided the results and shows that, across all countries, AZE, GEO, JPN, TJK, TUN, UK, and US demonstrate structural breaks in their DCCs. Specifically, a single break point is identified in DCCs for AZE (August 2008), TJK (April 2008), the UK (October 2009), and the US (May 2018). In addition, four significant structural breaks are detected for GEO (August 2008, June 2012, July 2014, and February 2017) and JPN (November 2008, September 2011, October 2015 and November 2017). Five significant breaks were observed in DCCs for TUN (September 2008, November 2010, December 2012, January 2015 and March 2017). These results reveal some close break dates in these countries, suggesting that structural changes for DCCs took place simultaneously around specific periods. In particular, we can allocate these break dates into four groups depending on the common features of the break periods. The first group of break dates corresponds to the period of the 2007–2008 food and financial crisis, when the international beef prices showed violent fluctuations from mid-2007 throughout 2008. The second group of break dates covers the period from 2009 to 2012, which can be recognised as the post-crisis adjustment period. The third group can be considered in the period 2014–2015 and the final group is the most recent period, 2017–2018.

To examine the changing phases of dynamic price transmission, we follow the procedure of Kalbaska and Gatkowski (2012) and apply the AR (1) model with dummy variables, as in the following equation:

where \(D\widehat CC_t^ \ast\) is the estimated pairwise correlation coefficient between IP and each domestic price in a beef-importing country. DMl,t is the dummy variable for structural break point l, for l = 1, \(\ldots \, ,\) n and where n denoted the number of break points detected by the Bai–Perron test in Table 9.

Table 10 reports the estimation results of the AR (1) model. First, except for GEO, the coefficients of AR (1) terms (ω1) are all positively significant at the 1% level for all the countries. These results indicate that one period past DCCs significantly affects the current DCCs for most countries. Second, we note that the coefficients of the structural change dummies (ζl) are statistically significant for all countries. Specifically, for the first group of break dates, the DCCs of AZE and GEO substantially decrease during the 2007–2008 food and financial crisis period, as indicated by the negative estimated coefficient of the dummy variable. In contrast, we can observe the significantly positive structural break dummies for JPN and TUN, suggesting that the DCCs of these two countries substantially increased at the beginning of the crisis period. In the second group, which is considered as the post-crisis adjustment period, DCCs increase in UK and GEO, as witnessed by the positive coefficient of corresponding dummy variables. JPN, however, shows negative DCCs after the second break date. For TUN, there are decreases in DCCs after the second break and an additional increase in DCCs from the third break. As the third group in the period 2014–2015, we can observe that the structural break dummies are negative for GEO and JPN, and these imply that DCCs decrease during this period. The positive dummy variable for TUN indicates a rise in DCCs around the beginning of 2015. Finally, for the most recent break points at 2017 and 2018 in group four, positive dummy variables can be detected for GEO, JPN and the USA, which confirms that DCCs increase in this period. In contrast, we find a negative coefficient of the dummy variable for TJK and TUN, reflecting that DCCs decreased after the first and fifth breaks in these two countries, respectively. Moreover, results of an LM Breusch–Godfrey (B–G) test for assessing residual autocorrelation, and an ARCH test, which evaluates the presence of conditional heteroskedasticity, suggest that the AR (1) model is suitably specified in all cases.

These findings suggest evidence that structural breaks play a crucial role in forecasting the future trends of interaction between global and local beef markets. Many structural changes in DCCs are identified between 2008 and 2009 surrounding the global food crisis. At that time, the DCCs in beef-importing countries show extreme volatility, reaching high levels during the crisis. This implies that the interconnectivity between international and regional markets is strengthened, and that the lag-lead relationships between international and regional markets are not constant over time, with DCCs showing both positive and negative values in a short span of time. The regression result with structural change dummy variables suggests that structural breaks affect the inter-linkages between world and local price volatilities positively or negatively, which allows for estimating more accurate DCCs.

Conclusions and discussions

This work analysed beef price volatility passthroughs between global and local markets for nine importing nations using DCC-GARCH-based models with a focus on identifying structural breaks in the models. The main results are that (1) local beef price returns for Azerbaijan, Georgia, Japan, Kazakhstan, Kyrgyzstan, Tajikistan, the UK and the United States have a structural change in mean or variance, all of which appear after 2010, (2) the global price Granger-causes indigenous prices in both mean and variance for Georgia, Tajikistan, and the United States, and no country showed price or price-volatility transmission from local to global prices, and (3) liaisons across world and regional markets regarding DCC are generally weak, but the intensity of market associations became more volatile around the 2008 global food crisis, which generated structural breaks during the period.

In our Granger linkage experiments, Georgia, Tajikistan, and the United States revealed more intimate connections with global prices. Self-sufficiency in beef for the three nations is not evidently low, and that of Japan is the lowest among the countries selected in our analysis, with 45%. Therefore, the degree of autarky seems to be irrelevant to the degree of interconnectivity between regional and world markets, at least according to these results. Note, however, that these findings are inconsistent with the outcomes in Guo and Tanaka (2020), where price volatility passthrough relies on the self-sufficiency rates of beef. Similarly, Guo and Tanaka (2019) examined the relationship between price volatility transmission and self-sufficiency in wheat. The authors concluded that higher self-sufficiency insulates domestic markets from international markets. Although it is widely believed that autarky policy measures stabilise local markets by protecting them from external shocks, Tanaka and Guo (2019) maintain that if domestic supply is more volatile compared with foreign supply, raising self-sufficiency could exacerbate domestic market steadiness.

Guo and Tanaka (2019) revealed that regional wheat prices in ten importing nations were unidirectionally Granger-caused by global wheat prices, which is consistent with our test results. However, their analysis differs from ours in the number of countries affected by international prices. In the paper, Granger causal relationships were identified for ten wheat importing nations, whereas Granger causality was detected for only five of nine beef-importing nations in our tests. This result may suggest that the interconnection between global and local beef markets is weaker than that of wheat markets. This weak linkage may be revealed in DCCs, whose means for beef and wheat are 0.10 and 0.17, respectively. The weak links for the beef sector also may be attributed to the flexible adjustment of the beef supply. Wheat supply heavily depends on climatic conditions, while beef supply can be more easily controlled by slaughtering domestic animals, which buffers shocks from foreign markets.

We gained the result that the connectivity between global and regional markets is intensified during the food price hikes between 2008 and 2009. This means that local markets are less likely to be affected by global market in the time of peace, but more sensitively receive shocks from a global catastrophe. Assuming that consumers have risk averse preference, national governmental bodies could implement trade restrictions such as export or/and import quotas or taxes to stabilize internal markets only in a stormy market period, which results in enhancing expected utility of consumers. However, they should not impose such regulations for market efficiency gains under usual conditions. This implication derived from the findings would be useful for policy makers who oversee local agricultural markets and market participants who want to procure beef or beef products at a steady price in local markets.

We demonstrated the first application of the time-variant procedure with structural break dummy variables to an international beef market linkage issue. As stated in the Introduction, though there are many publications concerning agricultural price spillovers, international beef price passthrough mechanisms are not fully understood. Despite this lack of knowledge, advanced econometric techniques have been developed that are helpful in deepening the understanding of agricultural price and price volatility transmissions, which is a topic for future research.

Data availability

The datasets generated and analysed in this study are available in the Global Information and Early Warning System repository: http://www.fao.org/giews/en/; and Bureau of Labor Statistics: https://data.bls.gov/pdq/SurveyOutputServlet; Office for National Statistics: https://www.ons.gov.uk/economy/inflationandpriceindices/datasets/consumerpriceindicescpiandretailpricesindexrpiitemindicesandpricequotes; Agriculture and Livestock Industries Corporation: https://www.alic.go.jp/english/; FRED: https://fred.stlouisfed.org/. The data that support the findings of this study can be obtained from the corresponding author upon request.

Notes

Developed by the US Census Bureau, X-13-ARIMA (autoregressive integrated moving average) is one of the most popular methods for seasonal adjustment.

Dickey and Fuller (1979).

Kwiatkowski et al. (1992).

We do not report the results of unit root tests for each price in levels for sake of brevity. Both the usual unit root tests and unit root tests with break show that all price series has unit root processes in their levels. These results can be obtained from the authors upon request.

This empirical technique has been widely applied in the examination of stock and commodity markets (see, e.g.).

The hats indicate suitable estimates of the corresponding quantitates.

Hong (2001) performed Monte Carlo experiments and suggested that the truncated kernel gives approximately similar power to non-uniform kernels such the Bartlett, Daniell, and QS kernels. In this paper, the truncated kernel was selected, which can provide compact support.

Nelson (1991) suggested that the EGARCH model not only ensures the nonnegative of coefficients in ARCH terms but also captures the presence of asymmetry in volatility.

See Glosten, Jagannathan and Runkle (1993) for details of the GJR-GARCH model.

A standard multiple linear regression model with m breaks (producing m + 1 regimes) can be expressed by \(Y_t = X_t^\prime \psi + Z_t^\prime \chi _j + \varepsilon _t\). Where \(t = T_{j - 1} + 1,...,T_j\) and j = 1, \(\ldots \,,\) m + 1. The Xt variables are those whose parameters do not vary across regimes, while the zt variables have coefficients that are regime-specific. For each m-partition (T1, \(\ldots \,,\) Tm), the parameter of ψ and χj is estimated by minimising the sum of squared residuals, denoted by \(S_T\left( {\widehat T_1,...,\widehat T_m} \right)\). Then, the estimated break dates \(\left( {\widehat T_1,...,\widehat T_m} \right)\) can be as \(\left( {\widehat T_1,\,...\,,\,\widehat T_m} \right) = \arg \min _{T_1,\,...\,,\,T_m}S_T\left( {\widehat T_1,\,...\,,\,\widehat T_m} \right)\).

See Cappelli et al. (2006) for an extensive analysis of these models’ advantages.

See Bollerslev and Wooldridge (1992).

BFGS (Broyden, Fletcher, Goldfarb, and Shannon) is a quasi-Newton optimisation method that uses information about the gradient of the function at the current point to calculate the best direction in which to find a better point.

Henceforth, the country abbreviation will be used (See Table 1).

In this study, each model is estimated by using the maximum likelihood method, and we determine the most suitable GARCH-type model according to the lowest SIC value and highest log likelihood ratio. In addition, the lag length k in the AR model, the ARCH term p, and the GARCH term q in the GARCH, GJR-GARCH, and EGARCH models are selected from among k = 1, 2, \(\ldots \,,\) 10, p = 1, 2, and q = 1, 2, respectively, by applying the SIC and residual diagnostics. Our results suggest that the AR (1) mean equation is chosen for each GAECH model.

The “leverage effect” is designed to capture the characteristic that the responses of conditional variance to positive and negative innovation differ. Specifically, bad news increases volatility more than good news.

These were estimated based on data from the FAOSTAT.

Japan presents the lowest self-sufficiency rate among the countries concerned, which is 45%.

We discuss more on the relationship between self-sufficiency and DCC in the Conclusion.

DCC, A-DCC, G-DCC, and AG-DCC model.

The results of the model estimation were not reported for sake of brevity. The results can be obtained from the authors upon request.

References

Abdelradi F, Serra T (2015) Food-energy nexus in Europe: price volatility approach. Energ Econ 48:157–167

Abdullah MA, Masih MMA (2016) Diversification in crude oil and other commodities: a comparative analysis. AAMJAF 12:101–128

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Econom 18:1–22

Bakucs LZ, Fertö I (2009) Marketing and Pricing Dynamics in the Presence of Structural Breaks: The Hungarian Pork Market. J int food agribus mark 21(2–3):116–133

Basher SA, Sadorsky P (2016) Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GOGARCH. Energy Economics 54:235–247

Boetel B, Liu DJ (2010) Estimating structural changes in the vertical price relationships in US beef and pork markets. J Agr Resour Econ 35(2):228–244

Bollerslev T, Wooldridge JM (1992) Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariances. Economet Rev 11(2):143–172

Cappiello L, Engle RF, Sheppard K (2006) Asymmetric Dynamics in the Correlations of Global Equity and Bond Returns. JFEC 4:537–572

Ceballos F, Hernandez MA, Minot N, Robles M (2017) Grain price and volatility transmission from international to domestic markets in developing countries. World Dev 94:305–320

Chang HS, Griffith G (1998) Examining long-run relationships between Australian beef prices. Aust J Agric Resour Econ 42(4):369–387

Cheung YW, Ng LK (1996) A causality-in-variance test and its application to financial market prices. J Econometr 72:33–48

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Dong X, Waldron S, Brown C, Zhang J (2018) Price transmission in regional beef markets: Australia, China and Southeast Asia. Emir J Food Agric 30(2):99–106

Engle R (2002) Dynamic conditional correlation – A simple class of multivariate GARCH models. J Bus Econ Stat 20(3):339–350

Fousekis P, Katrakilidis C, Trachanas E (2016) Vertical price transmission in the US beef sector: evidence from the nonlinear ARDL model. Econ Model 52:499–506

Ghoshray A (2011) Underlying trends and international price transmission of agricultural commodities. ADB Economics Working Paper Series, No. 257.

Gjika D, Horvath R (2013) Stock market comovements in Central Europe: evidence from the asymmetric DCC model. Econ Model 33:55–64

Glosten L, Jagannathan R, Runkle DE (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks. J Financ 48(5):1779–1801

Goodwin BK, Holt MT (1998) Price transmission and asymmetric adjustment in the US beef sector. Research Bulletin 4–99, Research Institute on Livestock Pricing Agricultural and Applied Economics, Virginia Tech

Gomez-Gonzalez JE, Rojas-Espinosa W (2019) Detecting contagion in Asian exchange rate markets using asymmetric DCC-GARCH and R-vine copulas. Econ Syst 43:100717

Griffith GR, Piggott NE (1994) Asymmetry in beef, lamb and pork farm-retail price transmission in Australia. Agr Econ 10(3):307–316

Guo J (2014) Causal relationship between stock returns and real economic growth in the pre- and post-crisis period: evidence from China. Appl Econ 54:12–31

Guo J (2018) Co-movement of international copper prices, China’s economic activity and stock returns: structural breaks and volatility dynamics. Glob Finance J 36:62–77

Guo J, Tanaka T (2019) Determinants of international price volatility transmissions: the role of self-sufficiency rates in wheat-importing countries. Pal Commun 5:1–13

Guo J, Tanaka T (2020) The effectiveness of self-sufficiency policy: international price transmissions in beef markets. Sustainability 12:6073

Hernández-Villafuerte K (2008) The Role of Asymmetric Price Transmission and Structural Breaks in the Relationship between Costa Rican Markets of Livestock Cattle, Beef and Milk. International Association of Agricultural Economists Conference. Available at http://ageconsearch.umn.edu/record/51697/files/Price%20Transmission-Costa%20Rican%20Markets%20of%20Livestock%20Cattle_%20Beef%20and%20Milk.pdf

Hou Y, Li S, Wen F (2019) Time-varying volatility spillover between Chinese fuel oil and stock index futures markets based on a DCC-GARCH model with a semi-nonparametric approach. Energ Econ 83:119–143

Hong Y (2001) A test for volatility spillover with applications to exchange rates. J Econometrics 103:183–224

Hwang E, Min HG, Kim BH, Kim H (2013) Determinants of stock market comovements among US and emerging economies during the US financial crisis. Econ Model 35:338–348

Kalbaska A, Gatkowski M (2012) Eurozone sovereign contagion: evidence from the CDS market (2005–2010). J Econ Behav Organ 83:657–673

Kaushik N (2018) Do global oil price shocks affect Indian metal market? Energy Environ 29:891–904

Kenourgios D, Naifar N, Dimitriou D (2016) Islamic financial markets and global crises contagion or decoupling? Econ Model 57:36–46

Kouyaté C, vonCramon-Taubadel S (2016) Distance and border effects on price transmission: a meta-analysis. J Agric Econ 67:255–271

Kwiatkowski D, Phillips PCB, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root. J Econometr 54:159–178

Lamoureux CG, Lastrapes WD (1990) Persistence in variance structural change and the GARCH model. J Bus Econ Stat 8:225–234

Ljung GM, Box GEP (1978) On a measure of lack of fit in time series models. Biometrika 65:297–303

Lloyd TA, McCorriston S, Morgan CW, Rayner AJ (2006) Food scares, market power and price transmission: The UK BSE crisis. Eur Rev Agric Econ 33(2):119–147

Mensi W, Beljid M, Boubaker A, Managi S (2013) Correlations and volatility spillovers across commodity and stock markets: Linking energies, food, and gold. Econ Model 32:15–22

Mollick AV, Assefa TA (2013) US stock returns and oil prices: The tale from daily data and the 2008–2009 financial crisis. Energ Econ 36:1–18

Naeem MA, Balli F, Shahzad SJH, deBruin A (2020) Energy commodity uncertainties and the systematic risk of US industries. Energ Econ 85:104589

Nelson DB (1991) Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59:347–370

Newey WK, West KD (1994) Automatic lag selection in covariance matrix estimation. Rev Econ Stud 61:631–653

Okorie DI, Lin B (2020) Crude oil price and cryptocurrencies: evidence of volatility connectedness and hedging strategy. Energ Econ 87:104703

Pan Z, Wang Y, Liu L (2016) The relationships between petroleum and stock returns: an asymmetric dynamic equi-correlation approach. Energ Econ 56:453–463

Perron P (1997) Further evidence on breaking trend functions in macroeconomic variables. J Econom 80:355–385

Pozo VF, Schoroeder TC, Bachmeier LJ (2013) Symmetric price transmission in the US beef market: New evidence from new data. Proceedings of the NCCC-134 Conference on Applied Commodity Price Analysis, Forecasting, and Market Risk Management, St. Louis http://www.farmdoc.illinois.edu/nccc134. Accessed 15 July 2020

Rizvi SAR, Arshad S (2014) An empirical study of Islamic equity as a better alternative during crisis using multivariate GARCH DCC. Islam Econ Stud 22:159–184

Sadorsky P (2014) Modeling volatility and correlations between emerging market stock prices and the prices of copper, oil and wheat. Energ Econ 43:72–81

Saghaian SH (2007) Beef safety shocks and dynamics of vertical price adjustment: the case of BSE discovery in the US beef sector. Agribusiness 23(3):333–348

Sanjuán AI, Dawson PJ (2003) Price transmission, BSE and structural breaks in the UK meat sector. Eur Rev Agric Econ 30:155–172

Shahzad SJH, Ferrer R, Ballester L, Umar Z (2017) Risk transmission between Islamic and conventional stock markets: a return and volatility spillover analysis. Int Rev Financ Anal 52:9–26

Shahzad SJH, Bouri E, Roubaud D, Kristoufek L (2020) Safe haven, hedge and diversification for G7 stock markets: gold versus bitcoin. Econ Model 87:212–224

Shiferaw YA (2019) Time-varying correlation between agricultural commodity and energy price dynamics with Bayesian multivariate DCC-GARCH models. Phys A 526:120807

Tamakoshi G, Hamori S (2013) An asymmetric dynamic conditional correlation analysis of linkages of European financial institutions during the Greek sovereign debt crisis. Eur J Financ 19(10):939–950

Tamakoshi G, Hamori S (2014) Co-movements among major European exchange rates: a multivariate time-varying asymmetric approach. Int Rev Econ Finance 31:105–113

Tanaka T, Guo J (2020) How does the self-sufficiency rate affect international price volatility transmissions in the wheat sector? Evidence from wheat-exporting countries. Humanit Soc Sci Commun 7:26

Tanaka T, Guo J (2019) Quantifying the effects of agricultural autarky policy: resilience to yield volatility and export restrictions. J Food Secur 7(2):47–57

Tissaoui K, Azibi J (2019) International implied volatility risk indexes and Saudi stock return-volatility predictabilities. N Am J Econ Financ 47:65–84

Vacha L, Barunik J (2012) Co-movement of energy commodities revisited: evidence from wavelet coherence analysis. Energ Econ 34:241–247

Xu H, Hamori S (2012) Dynamic linkages of stock prices between the BRICs and the United States: effects of the 2008–09 financial crisis. J Asian Econ 23:344–352

Xu W, Ma F, Chen W, Zhang B (2019) Asymmetric volatility spillovers between oil and stock markets: evidence from China and the United States. Energ Econ 80:310–320

Zhang YJ, Chevallier J, Guesmi K (2017) ‘De-financialization’ of commodities? Evidence from stock, crude oil and natural gas markets. Energ Econ 68:228–239

Zivot E, Andrews DWK (1992) Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J Bus Econ Stat 10:251–270

Acknowledgements

The research of the second author is in part supported by a Grant-in-Aid from the Japan Society for the Promotion of Science (Grant Number (A)20K15613).

Author information

Authors and Affiliations

Contributions

TT and JG designed the research. TT conceived the study with inspiration from his previous studies. TT also performed the background of the paper and discussed the policy implications of the empirical results. JG constructed the econometric model and edited the program code for analyzing. JG also analyzed and interpreted the data regarding the common determinants of wheat price volatility transmission from international to local markets in wheat-importing countries. The authors equally contributed to this work.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Tanaka, T., Guo, J. International price volatility transmission and structural change: a market connectivity analysis in the beef sector. Humanit Soc Sci Commun 7, 166 (2020). https://doi.org/10.1057/s41599-020-00657-x

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-020-00657-x